Before I designed a single screen for KwikPay, I moved to Kuwait.

Not for a research trip. Not for a two week sprint. I relocated. Because the brief did not exist yet and I knew I could not write it from a desk in India.

The product we were building had no comparable reference in the market. No local case study to learn from. No user research to inherit. No competitor who had solved this before.

The only way to understand what needed to be built was to go where it needed to work.

A problem well stated is a problem half solved. — Charles Kettering

The Market Nobody Had Mapped

Kuwait looks like a clean fintech opportunity on paper.

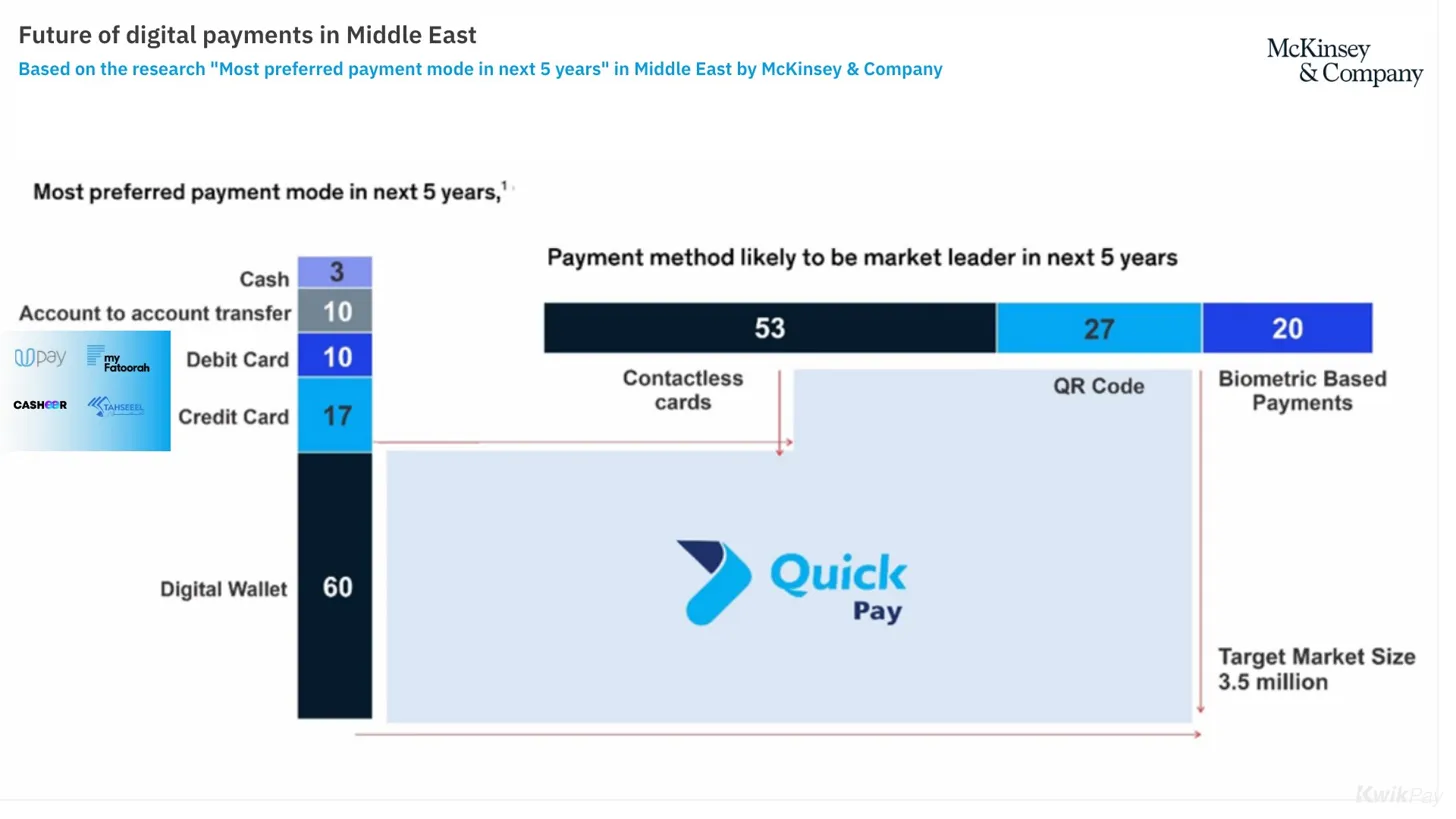

4.8 million people. High smartphone penetration. A McKinsey study pointing to digital wallets as the most preferred payment mode in the Middle East within five years. A target addressable market of 3.5 million users. 60% of surveyed people saying they would prefer to pay digitally.

Then you land. And the paper stops making sense!

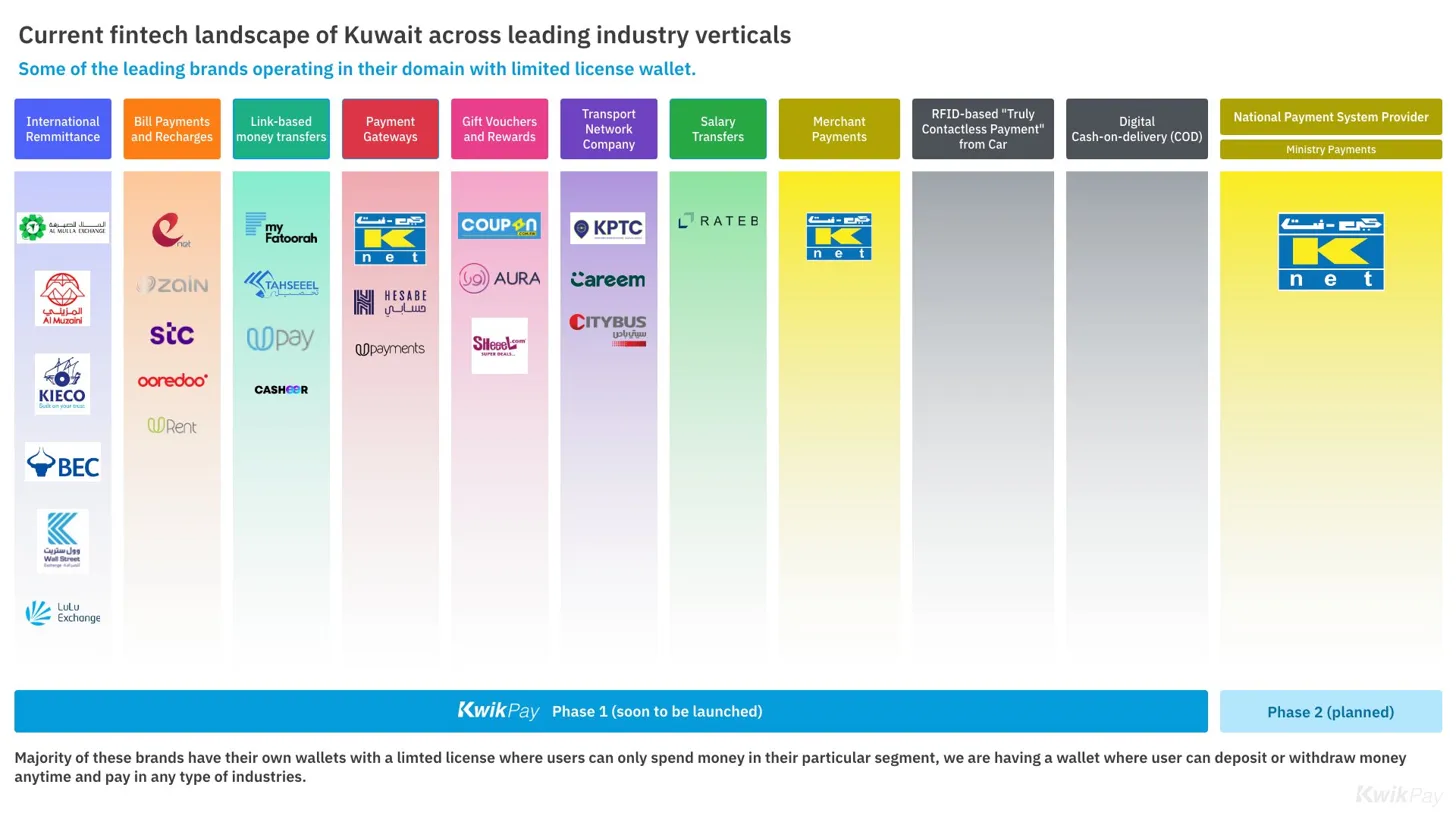

Cash is everywhere. Merchants do not accept cards. Delivery apps run entirely on cash on delivery. And the few digital payment products that exist are all locked inside their own walls. Zain's wallet works for Zain. KPTC's wallet works for transport. Talabat wallet works for Talabat Nobody had built something that worked everywhere, for everyone, across every category.

That was the whitespace. Not because nobody had seen it. Because nobody had built the infrastructure to fill it.

KwikPay was going to be the first.

But the real question was not whether the market existed. It was whether people were actually ready to change how they paid. And that question could not be answered by a slide.

Getting Into the Field

I did not start with a research framework. I started with conversations.

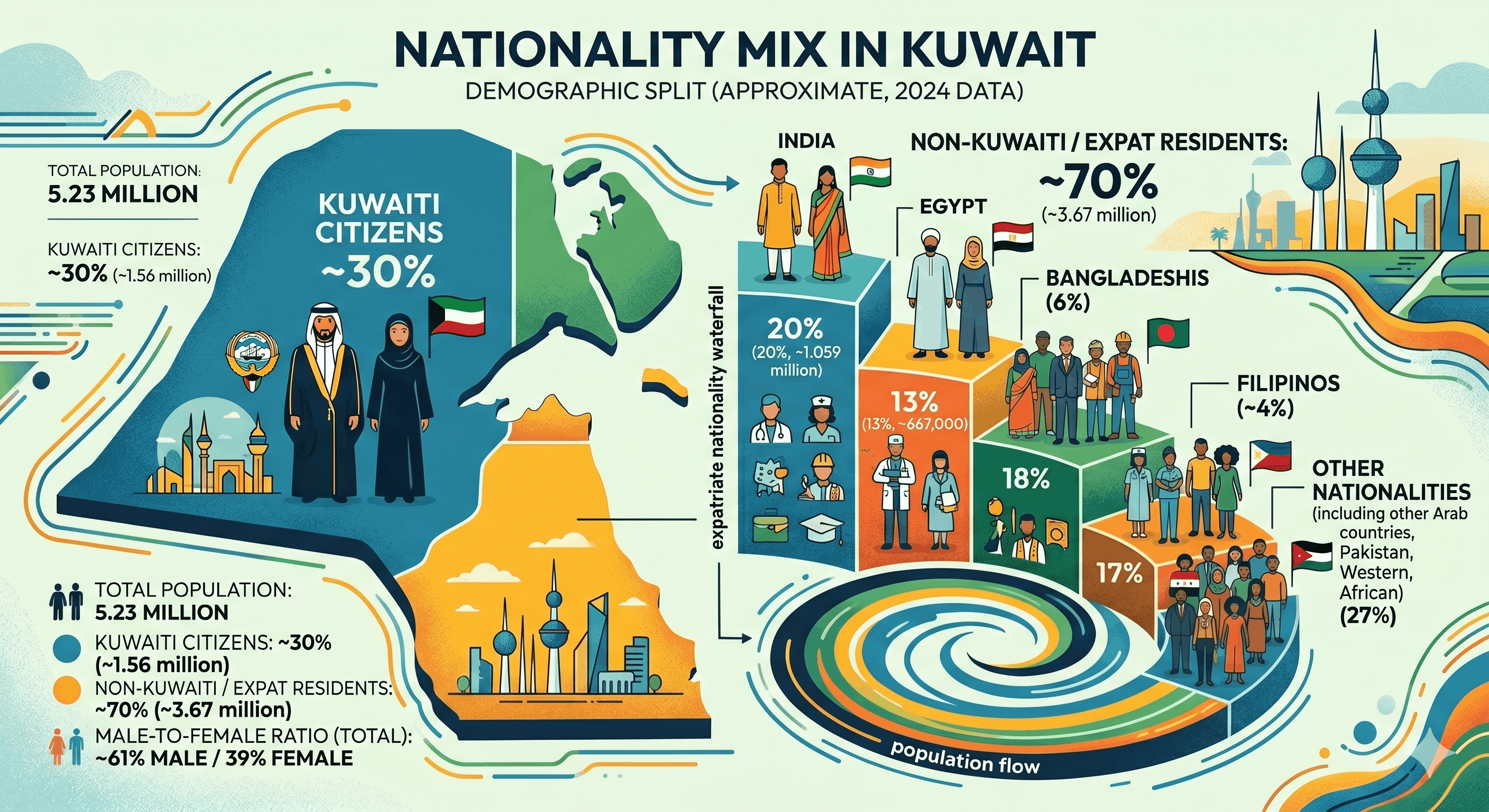

Over the first few weeks in Kuwait, I spoke to people from every major nationality in the country. Indian, Pakistani, Bangladeshi, Filipino, Arabs, native Kuwaiti. Each community had a completely different relationship with money. Different sending patterns. Different spending habits. Different levels of trust in digital products.

I also spent a significant amount of time on the merchant side. Not just large businesses. I walked into small baqalas (grocery shops), talked to restaurant owners, taxi drivers, online sellers running their entire business through Instagram and Snapchat. I wanted to understand what payment acceptance actually looked like at ground level, not just what the market reports said about it.

What I was really trying to find was the nerve of the problem. Not the surface friction but the deeper reason why a market with this much digital readiness was still so dependent on cash.

That answer took a few weeks to fully surface. But it started becoming clear the moment I sat down with the first merchant.

The User Side: Lifecycle and Spend Patterns

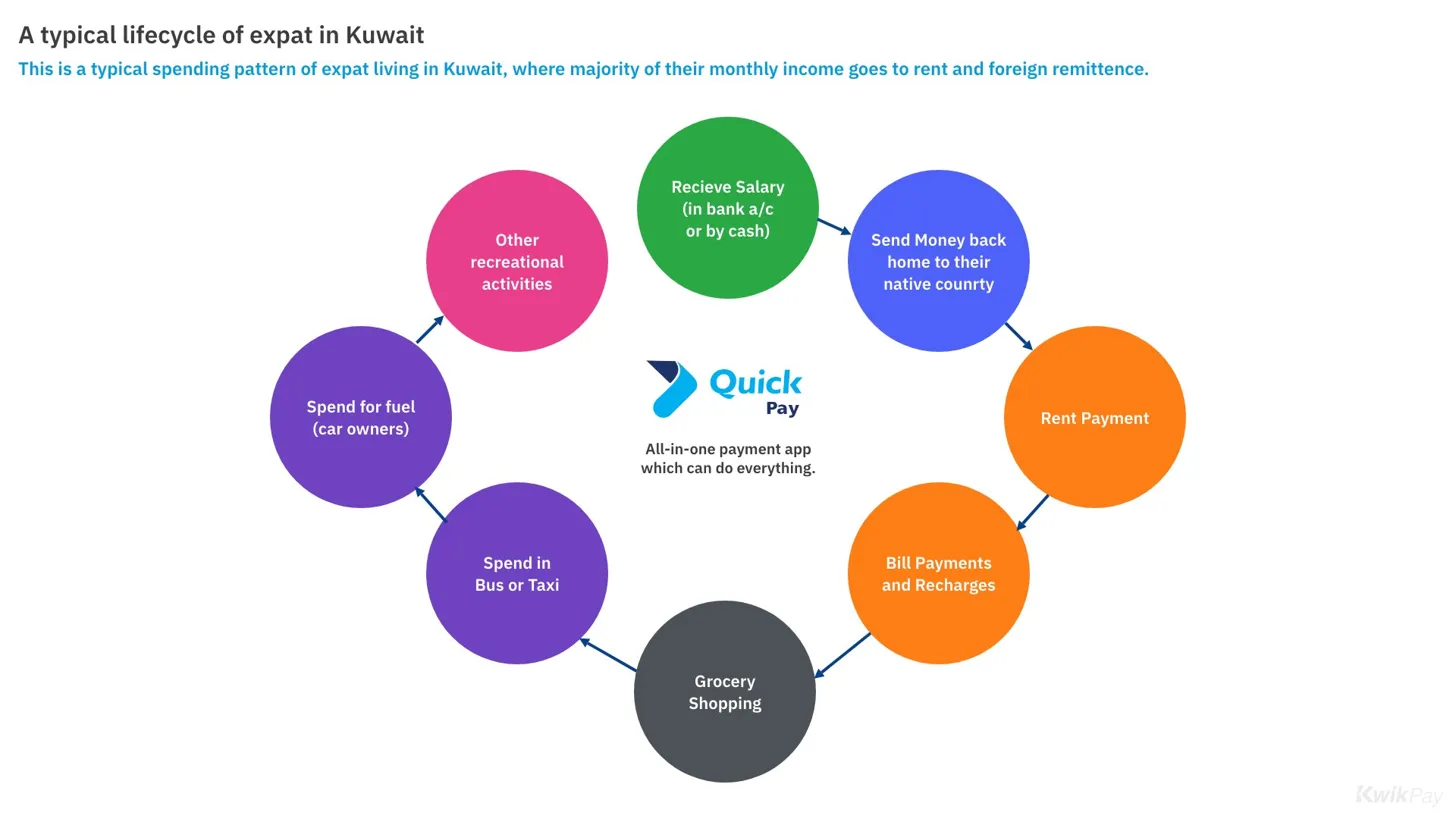

The expat population in Kuwait follows a remarkably predictable financial cycle.

Salary comes in. Remittance goes out first, almost immediately, sent back home to family. Then rent. Then utility bills and phone recharges. Then groceries, transport, fuel. Whatever is left goes to recreation and leisure. Month after month, the pattern repeats with very little variation.

What this told me was not just how expats spent money. It told me where the anxiety lived. Remittance was the highest priority and also the most painful to execute. Bank transfers were slow, expensive, and required navigating systems that were often not built with expats in mind. That was a direct product opportunity.

Native Kuwaitis had a completely different pattern. Higher disposable income. Stronger brand affinity. A deeply ingrained culture around loyalty points and rewards, driven by years of existing businesses conditioning them to expect it. Companies like Aura had built entire ecosystems around this behaviour.

Two audiences. Two completely different motivations for using a digital wallet. That distinction ended up shaping how we thought about product positioning and feature prioritisation from the very beginning.

The Merchant Side: What the Ground Actually Looked Like

The merchant conversations were the most revealing part of the entire research process.

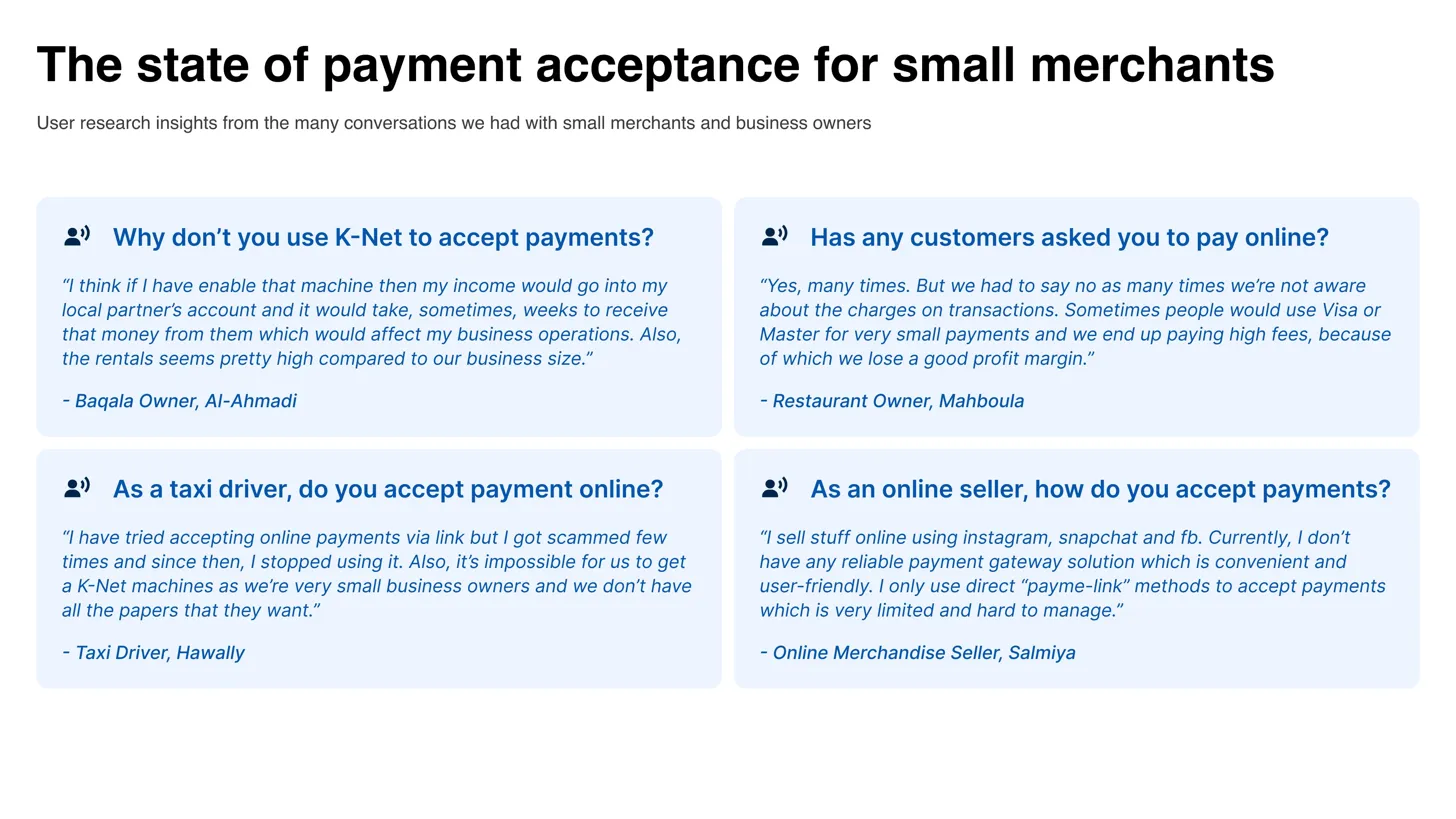

Every merchant I spoke to had a version of the same problem. The existing payment infrastructure was built for large businesses. For a small baqala owner or a taxi driver or someone selling on Instagram, accepting digital payments was more trouble than it was worth.

The K-Net machine, which was the dominant payment terminal in Kuwait, came with a significant catch. For many small business owners, enabling it meant routing income through a local partner's account. That money could take weeks to arrive. For a business running on thin margins, that was not a delay they could absorb.

Transaction fees compounded the problem further. A restaurant owner told me directly that customers would sometimes pay with a Visa or Mastercard for a very small amount and the fee would wipe out the profit margin on that transaction entirely.

Taxi drivers had stopped accepting digital payments altogether after being scammed through link based payment methods. Online sellers were managing their entire payment flow manually through direct links, with no dashboard, no reporting, no way to track what was coming in.

The infrastructure existed. But it had been designed without these people in mind. And they were a significant part of the market.

Three Observations That Told Us How This Market Wanted to Pay

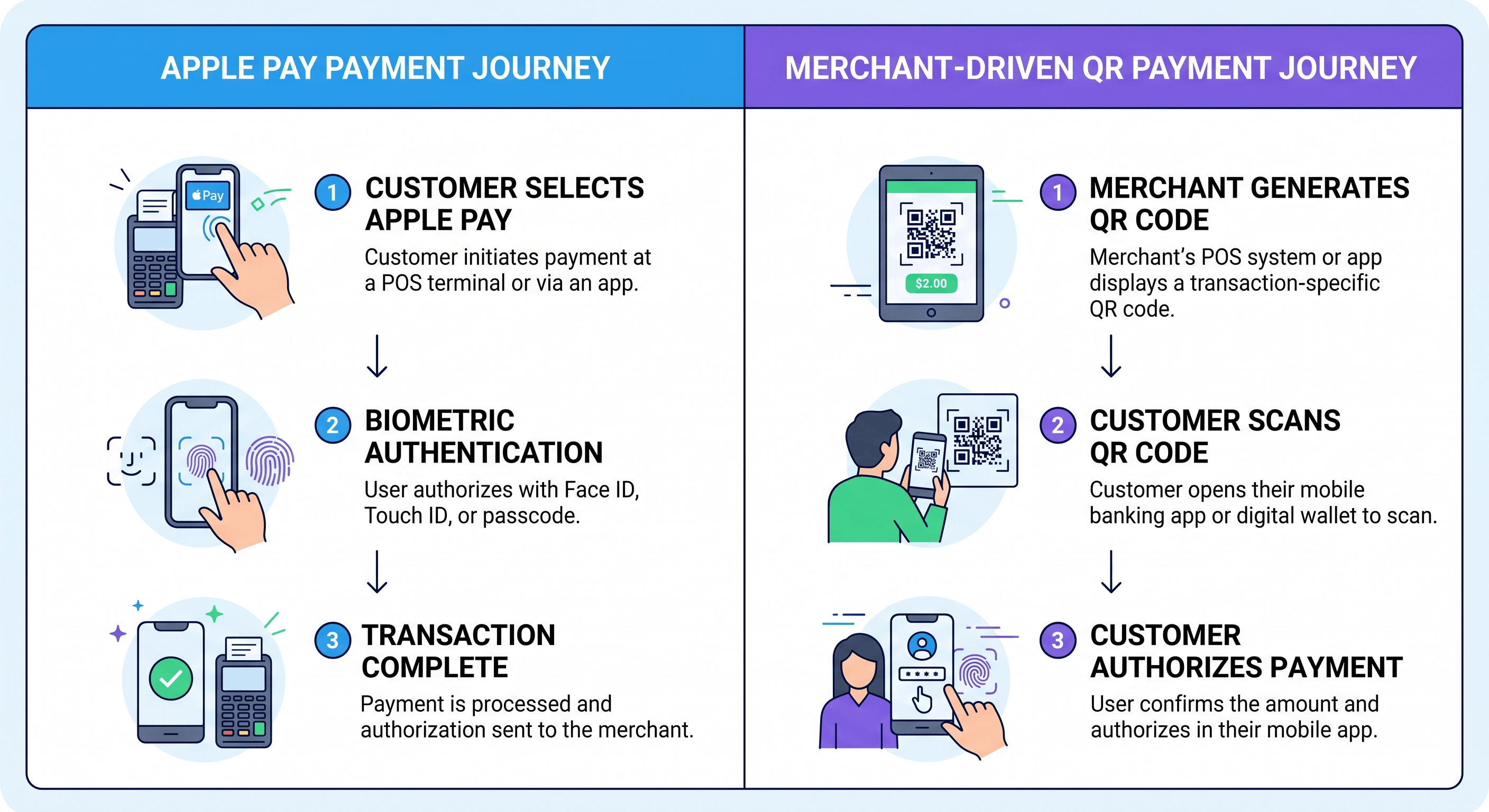

Not every insight comes from a research session. Some come from just living in the market long enough to notice what nobody is documenting. K-Net was the incumbent. Slow, expensive, friction heavy. Easy to position against. But Apple Pay was a different kind of threat entirely. It was faster than any QR based flow we could build. It was already trusted. It was already on every iPhone in the country. And the people most likely to adopt KwikPay were the same people already using it.

01 — Apple Pay was the real competitor, not K-Net

Apple Pay was faster than any QR flow we could build, already trusted, already on every iPhone in the country. Competing with it on speed was not a battle worth fighting. But it had two structural gaps. It was linked directly to a primary bank account, and it gave users no control over how or when it was used. That told us exactly where to position KwikPay: not as a faster payment method, but as a safer, more controlled secondary wallet. It also told us something about the interaction model. If users were already comfortable with merchant initiated tap payments, we could flip our core flow from user driven to merchant driven and it would feel natural rather than foreign.

02 — A lost card and a banking system with no middle ground

I lost over 50 KWD because a lost card was used before I could block it. But the more revealing part was what happened when I opened my banking app to do something about it. The only options were block the card entirely or leave it exposed entirely. No way to pause tap to pay. No way to set a spend limit. No way to restrict specific merchant types. The infrastructure existed but the control layer did not. For a market this dependent on physical cards, that gap was significant and nobody had built anything to fill it.

03 — When 500 fils is not a small difference

500 fils is the smallest meaningful unit of currency in Kuwait. One Kuwaiti Dinar has 1000 fils, which means 500 fils is half a dinar, roughly $1.63, enough to buy a moderate breakfast. To put it in payment terms, the difference between 5.250 KWD and 5.750 KWD is exactly that. Not a rounding error. A real amount that real people notice. In a market where people think and transact at that level of precision, any payment flow that asks a user to manually enter an amount is introducing real risk. One digit off and the trust breaks. That single observation made the case for merchant driven payments clearer than any user interview could have. If the merchant initiates the amount, the user only needs to confirm. The precision problem disappears entirely. This behaviour also shaped a hardware decision. If the merchant was going to own the payment initiation, the device in their hand needed to make that as seamless as possible. It pointed us directly toward sourcing a dynamic QR soundbox where the merchant triggers the request and the customer simply confirms. The interaction model and the hardware decision came from the same insight.

What the Research Changed

Good research does not just validate assumptions. It replaces them.

By the end of the immersion period, three things had shifted significantly from where the product started.

The positioning changed.

KwikPay was no longer trying to be a primary payment method. It was a secure secondary wallet. Separate from your bank. Controllable. Capped. A place to keep a specific amount for daily spending without exposing your entire account to every tap.

The core interaction model changed.

The original flow was user initiated. Open app, scan QR, pay. But given how precise Kuwaitis are about amounts, and how much friction even a small error creates, we shifted to a merchant driven model. The merchant initiates the payment request. The user confirms. That single change reduced the cognitive load on the user side and removed the risk of amount entry errors entirely.

A feature found its bigger self.

Standing in a queue at a fuel pump in Kuwait in summer is not just inconvenient. It is physically unpleasant. The heat is extreme. Winding down a car window for thirty seconds ruins the entire climate controlled environment you have been maintaining. I watched this happen repeatedly. People visibly uncomfortable, doing it anyway because there was no other option.

There was already an RFID tag feature in the product roadmap. The mechanic was simple: a tag glued to the car, scanned by the boom barrier or fuel pump attendant, which triggered a payment approval notification on the user's app. The user confirms from inside the car without rolling down the window, without any physical interaction at all.

Functional, practical, useful. But spending time with native Kuwaitis revealed something that a feature spec could never capture. Cars here are not just transport. They are an extension of identity. The model, the condition, the accessories — all of it carries social weight. People take pride in their cars in a way that is specific to this culture and this market.

That observation changed the question entirely. Not "how do we make this RFID feature work well" but "what if this feature deserved its own product identity, its own branded space, its own emotional language." That reframe is where KwikPass began to take shape. The execution of what it became is a different story, and it is the one that next case study tells.

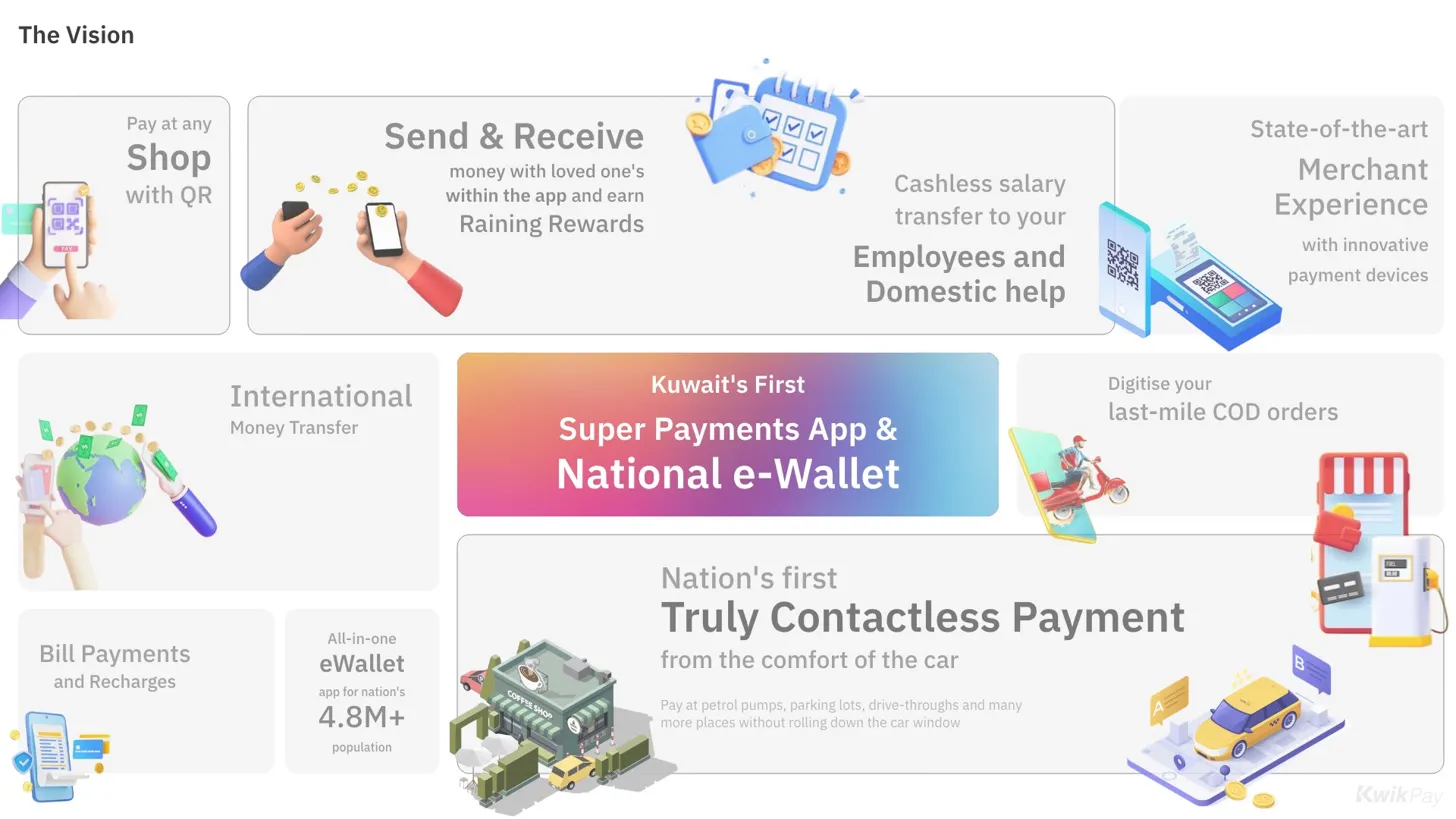

The opportunity map: A market way bigger than the brief

And beyond the product itself, the research mapped where KwikPay could grow.

Delivery platforms running entirely on cash on delivery were a direct integration opportunity. The COD model exists because customers want to see and check a product before paying. But for standard deliveries, a Digital COD model where payment is triggered on delivery confirmation rather than upfront could bridge that trust gap without asking people to abandon familiar behaviour entirely.

Public transport, ride hailing, parking, fuel, retail shopping. Each one a vertical where the payment experience was broken, missing or stuck on outdated infrastructure. Each one a surface where a full license wallet had a clear right to play.

The McKinsey data gave us the macro confidence. The ground research gave us the sequencing logic. Which verticals to prioritise, which audience to acquire first, and what behaviour to work with rather than against. That is the part no research report could have given us.

Research in the Chaos: What This Process Taught Me

I did not come to Kuwait with a research plan. I came with a question: what does this market actually need, and why has nobody built it yet.

There was no screener. No recruited participants. No incentive budget.

The research happened in markets, at fuel pumps, inside small shops, in conversations with taxi drivers who had been scammed and restaurant owners who had given up on digital payments entirely. The methodology, if you could call it that, was simply being present and paying attention.

A few things became clear about doing research this way.

Chaos is data if you know how to read it.

There was no shortage of signal. The problem was that it came from everywhere at once — different nationalities, different economic realities, different relationships with money and technology. The discipline was not in generating insights but in knowing which ones were structural and which were surface level. The ones that mattered kept appearing across completely different conversations with completely different people.

The best insights came from living the friction, not just observing it.

Losing 50 KWD to a lost card. Standing in a fuel pump queue in extreme heat. Trying to pay on a delivery app and defaulting to cash because nothing else felt trustworthy. These were not research activities. They were just life in this market. But they produced more useful product direction than any structured session could have.

Research without a brief requires you to know when to stop.

When there is no PM defining the scope and no research plan setting the boundaries, the risk is that you keep going indefinitely. The discipline I had to build was recognising when a pattern had appeared enough times to act on. When three different merchants described the same problem in three completely different ways, that was the signal to stop collecting and start synthesising.

The market will tell you what it needs if you are present enough to hear it.

Every product decision that came out of this research — the secondary wallet positioning, the merchant driven interaction model, the KwikPass reframe — came from something observed in the field, not something hypothesised at a desk. That is not a repeatable process you can document in a template. It is a way of working that only functions when you are fully inside the context you are designing for.

This is where the brief finally existed. What we built with it is the next story — see you there.